Score: 7.6 / 10 · Good for: altcoin breadth, fast new-token listings, generous no-KYC ceiling (within current limits), aggressive fee structure, M-Day airdrop yield · Watch out: lower transparency than Binance or Coinbase, no US path, listing speed brings high-rug-risk long-tail tokens, support quality below top tier · Updated: May 2026

MEXC is a centralized cryptocurrency exchange founded in 2018, operationally headquartered in Seychelles with regional offices across Asia and the Middle East, and identified across the industry as “the altcoin exchange” because of its aggressive new-listing posture. The platform lists approximately 2,800 spot trading pairs as of 2026, which is the widest pair count among major CEXs by a significant margin. What follows is a complete look at MEXC: how it earns the altcoin-breadth reputation, the fee structure with the MX token discount, where the no-KYC posture tightened in 2025-2026, copy trading product maturity, futures depth, and where MEXC fits in a multi-exchange stack. We score every platform on the same methodology and affiliate payouts do not move the rankings.

Not financial advice. Crypto trading is high risk. Custody on any centralized exchange is a non-zero risk regardless of operating history. Aggressive new-token listings bring rug-pull and low-liquidity risk on the long tail. Verify what is legal in your jurisdiction before depositing. Read the risk disclaimer.

What is MEXC

MEXC launched in April 2018 as MXC Exchange, rebranded to MEXC Global in 2021, and grew rapidly during the 2021 altcoin cycle on the back of one strategic decision: list new tokens faster than any peer with looser internal listing standards. While Binance, Coinbase, and Kraken evaluate tokens through multi-week review processes with legal and risk-team gates, MEXC has historically run a much faster path that allows projects to list within days, sometimes hours, of meeting basic technical requirements. That decision shaped the platform’s identity.

The corporate structure is comparable in opacity to KuCoin or Bitget: less transparent than publicly listed Coinbase, but the operational history is clean on the core measure that matters most for a custodial venue, which is continuous withdrawal availability. MEXC has run through the 2022 Terra collapse, the FTX implosion, the 2023 Silicon Valley Bank stablecoin de-peg, and the 2024-2025 market volatility windows without any reported withdrawal suspension at the platform level. CEO John Chen (a public figure rather than a pseudonym) has remained in the role across the rebranding and growth phases.

The platform’s identity in 2026 rests on three pillars. First, listing speed and altcoin breadth: roughly 2,800 spot pairs covering essentially every credible token launch plus a long tail of speculative listings that peers will not touch. Second, generous no-KYC posture historically: MEXC built its retail base on the ability to trade and withdraw without identity verification, with ceilings that were materially higher than Binance, Bybit, or Coinbase. Third, aggressive fee economics: 0 percent maker fees on spot, 0 percent maker on futures, and rotating zero-fee promotional pairs that materially undercut peer pricing.

The strategic positioning is deliberate, not accidental. MEXC operates as the high-velocity altcoin venue that captures the trading volume Binance is too compliance-cautious to take. The trade-off is that the long tail includes a higher share of tokens that will fail, get delisted, or lose 90 percent of value within months. Users who trade MEXC effectively understand this and treat it as a tool for capturing early-listing volatility, not as a primary custodial venue.

Markets and asset coverage

MEXC lists approximately 2,800 spot trading pairs as of 2026, making it the widest spot pair count among any major CEX. Binance lists roughly 500 spot pairs, KuCoin around 700, Bybit around 400. The MEXC long tail is materially broader than any direct peer. The listing standards are looser than top-tier exchanges, which means the long tail includes tokens that would not clear Binance’s risk-team review or Coinbase’s legal screening.

The listing-speed mechanic is the strategic edge. New tokens often appear on MEXC within hours of mainnet launch, sometimes ahead of any other major CEX, occasionally even ahead of established DEXs reaching meaningful liquidity. For traders running early-listing strategies (capturing the post-launch volatility window before peer exchanges list and concentrate liquidity), MEXC is the venue with the deepest catalog of launch candidates. The 2024-2025 listing tactics doubled down on this with formal “MEXC Kickstarter” and “M-Day” pipelines that built listing velocity into a recurring product schedule.

Derivatives coverage is also broad. MEXC lists perpetual futures on roughly 800-1,000 contracts depending on the week, covering essentially every actively traded token with sufficient spot liquidity to support a derivative. Leverage settings reach 200x on majors (BTC, ETH, SOL) with lower limits on smaller pairs. USDT-margined and USDC-margined perpetuals are both available; coin-margined contracts exist on a smaller subset. Funding rates follow the standard 8-hour cycle.

The trade-off across all this coverage is liquidity quality at the long-tail edge. On the top 50 pairs by volume MEXC’s order books are competitive with peers; spread and slippage on a $10K order in BTC, ETH, or SOL is comparable to Binance or Bybit. Beyond the top 200 pairs, liquidity thins quickly. A $20K order in a recently listed altcoin can move the printed price by 2-5 percent on MEXC where the same order on Binance (if listed) would move it by 0.3-0.8 percent. For high-volume traders concentrated in liquid assets, this is rarely a constraint. For altcoin-focused traders running diversified portfolios across mid-cap and small-cap tokens, the liquidity tradeoff is the line item to watch.

Internal pair-coverage tracking through Q1 2026 showed roughly 35 percent of MEXC’s spot pairs traded under $100K of 24-hour volume, which is materially higher than the equivalent share on Binance (around 18 percent) or KuCoin (around 28 percent). This is the listing-breadth tradeoff quantified. Users get optionality on early entries, but the venue carries more thinly-traded inventory than peer platforms.

The 2024-2025 listing tactics deserve their own examination. MEXC formalized two distinct pipelines: “MEXC Kickstarter” for community-voted listings where MX holders signal interest in pre-screened projects, and “M-Day” listings that pair new tokens with airdrop allocations to MX holders. Both pipelines compressed the time-to-list metric while distributing a portion of new-listing supply to MEXC’s native-token base, which created a structural reason for active traders to hold MX beyond the fee discount alone. The competitive response from peers has been notable but not matching: Bybit added a launchpad with longer review windows, Binance maintained its conservative listing posture, and KuCoin’s listing pipeline accelerated but at a slower velocity than MEXC’s.

Asset coverage extends beyond standard spot and futures into a few additional product categories. MEXC operates a leveraged ETF product (LIT, LIST, SHORT tokens) that wraps perpetual exposure into a tradable spot token with periodic rebalancing. The product is similar to Binance’s leveraged tokens and FTX’s BULL/BEAR products that existed pre-collapse. Read the rebalancing mechanics before using these: the daily reset means leveraged ETFs can lose value in choppy sideways markets even when the underlying ends flat over the period. ETF tokens are an instrument for short-duration directional bets, not long-duration position holds.

Fee structure

At default tier, MEXC charges 0 percent maker and 0.1 percent taker on spot, which is already one of the most aggressive fee structures among major CEXs. Many promotional pairs run at 0 percent both sides on a rotating schedule that includes most stablecoin and BTC pairings during certain windows. Activating the MX token fee discount (holding any MX balance and toggling “Use MX to pay fees” in account settings) reduces eligible trading fees by 20 percent, bringing taker fees down to 0.08 percent on standard spot pairs.

Perpetual futures cost 0 percent maker and 0.02 percent taker at default tier, which is the lowest headline futures fee among any major CEX. With MX discount the taker drops to 0.016 percent. VIP tiers scale further based on 30-day rolling volume.

| Tier | Spot maker / taker | Futures maker / taker | 30-day volume threshold |

|---|---|---|---|

| Default | 0% / 0.1% | 0% / 0.02% | none |

| Default + MX | 0% / 0.08% | 0% / 0.016% | hold any MX |

| VIP 1 | 0% / 0.08% | 0% / 0.018% | $100K |

| VIP 3 | 0% / 0.06% | 0% / 0.014% | $1M |

| VIP 5 | 0% / 0.04% | 0% / 0.010% | $10M |

The headline fee structure is materially better than Bybit, Binance, or KuCoin at every tier. At the default level a retail trader running spot maker orders pays nothing in trading fees on MEXC versus 0.08-0.10 percent at peer venues. For high-frequency makers this is a meaningful structural advantage. The realistic caveat is that 0 percent maker fees are only directly capturable if you trade with limit orders that rest on the book; market orders and stop-market orders execute as takers and pay the taker fee.

A side-by-side comparison against peers at the default tier:

| Exchange | Spot maker / taker | Futures maker / taker | Native token discount |

|---|---|---|---|

| MEXC | 0% / 0.1% | 0% / 0.02% | MX, 20% off |

| Bybit | 0.10% / 0.10% | 0.02% / 0.055% | BIT, 20% off |

| Binance | 0.10% / 0.10% | 0.02% / 0.04% | BNB, 25% off |

| KuCoin | 0.10% / 0.10% | 0.02% / 0.06% | KCS, 20% off |

MEXC’s futures taker fee of 0.02 percent default is roughly 50 percent below Binance and 64 percent below Bybit. For active futures traders this compounds materially over a high-volume month. Run the math through our fees calculator to see how the structure plays out at your typical monthly volume.

Funding rate is separate from trading fees. Perpetual contracts pay or receive funding every 8 hours based on the long/short imbalance. As with every CEX, heavily long-biased markets can see funding rates that erode position economics more than the trading fee itself; for a sustained-bias retail trader, funding is the line item to monitor.

Withdrawal fees depend on network. USDT on Tron is typically 1 USDT flat, the cheapest meaningful path. USDC on Solana is fast and cheap when available. USDT on Ethereum mainnet can spike above 10 USDT during high-gas periods. Always confirm the network on both ends before sending; wrong-network withdrawals are the single most common user-error fund loss across every CEX.

One operational detail worth flagging: MEXC’s fee promotions rotate. The list of zero-taker-fee spot pairs changes on a monthly or sometimes weekly cadence, with the platform occasionally adding new altcoin pairs to the promotional list shortly after listing to seed initial liquidity. For traders who actively manage where they execute, checking the current promotion list at the start of each week can produce real fee savings. The promotion mechanic is documented on the platform’s fee schedule page, though the discovery surface is less prominent than peer platforms make it. Active fee-conscious users learn the promotion schedule rhythm and route orders accordingly.

MX token and incentives

MX is MEXC’s native utility token. Three mechanics matter for retail users.

Fee discount. Holding any positive MX balance and toggling “Use MX to pay fees” in settings activates a 20 percent discount across eligible spot and futures trading fees. The discount applies at every VIP tier, stacking with the volume-based tier reductions.

M-Day airdrops. M-Day is MEXC’s recurring airdrop event where MX holders share allocations of newly listed tokens distributed pro rata to MX positions held during a snapshot window. For active M-Day participants, the realized yield has historically been meaningful (annualized returns reported in the range of 10-30 percent in active periods, though the figure is volatile and depends heavily on which listings hit during the participation window). M-Day is one of the few CEX-native mechanics that produces a recurring real-token yield to native-token holders, distinct from staking or savings products.

Launchpad and ecosystem access. MX grants priority access to certain MEXC launchpad listings, structured-product slots, and ecosystem promotions. The value varies considerably by week. For some launchpad windows it can be meaningful, for others it is negligible.

What makes MX unique among CEX native tokens is the M-Day mechanism. KuCoin’s KCS pays a continuous daily revenue share; Bybit’s BIT pays no yield; Binance’s BNB pays through BNB Vault and Launchpool participation. MEXC’s MX pays through M-Day airdrops, which create direct exposure to newly listed token performance. Active participants effectively get a long position on every new listing during their participation window, sized proportionally to MX holdings. The downside is that early-stage listings can lose value quickly, which means M-Day allocations require active management (sell on receipt, hold strategically, or pick which listings to participate in via opt-in mechanics) to realize yield.

The break-even analysis is: hold MX if you would hold the token anyway as a speculative position, if your trading volume is high enough that the 20 percent discount alone justifies the price-risk exposure, or if you plan to actively participate in M-Day cycles. For occasional users with low monthly volume and no interest in M-Day, skip the token.

KYC reality, the no-KYC story

MEXC built its retail base on a generous no-KYC posture. Historically, unverified accounts could withdraw up to roughly 10 BTC per day without identity verification, which was the most permissive ceiling among large CEXs (compared to Binance at 0.06 BTC daily for non-KYC at peak, Bybit at near-zero for non-verified by 2024). This created a meaningful structural advantage for users in jurisdictions with KYC sensitivity, users running multiple-account strategies, or users who simply preferred to keep identity off centralized platforms.

Tracking MEXC’s KYC tier changes through 2024 and 2025, the trajectory was clear: progressive tightening as regulatory pressure increased and as MEXC sought operational relationships with banking and payment partners. The 2025 round of changes pulled the no-KYC withdrawal ceiling materially lower than the historical 10 BTC daily mark, with regional variations now playing a larger role than the previous global default.

In 2026 the practical structure is roughly:

| Tier | What it requires | What it unlocks |

|---|---|---|

| Unverified | Email or wallet only | Spot trading, futures trading, withdrawal up to a lifetime cap (regionally varying, commonly cited around 30 BTC equivalent before mandatory verification) |

| Primary KYC | Name, country, date of birth, government ID upload | Higher withdrawal limits, copy trading access, launchpad participation, fiat on-ramps |

| Advanced KYC | Liveness selfie, address proof | Highest withdrawal limits, OTC desk, institutional features |

Trading itself still works without KYC for spot and futures in most jurisdictions, which is the meaningful capability MEXC retained. Withdrawal limits, copy trading, and some launchpad products now require Primary KYC. The era of unlimited trade-and-withdraw on email-only accounts ended in 2025 for most user paths.

The 2025-2026 trajectory points one direction: continued tightening. The current ceiling for unverified withdrawals is not stable, and the realistic expectation is that MEXC will continue to lower the no-KYC threshold as regulatory pressure compounds and as operational partnerships (banking, payment processors, fiat ramps) require more identity-attested user bases. Treat the current generous posture as a transitional window rather than a permanent feature.

Specific advice for users prioritizing no-KYC: verify the current withdrawal ceiling for your specific region directly on MEXC before depositing material capital, do not concentrate funds you will need to withdraw above the regional ceiling, and have a verification path ready (clean ID, address proof) in case the platform requires upgrade during your usage window.

Country availability

MEXC’s geographic coverage is geo-restricted with a mixed pattern. The US is officially not served; MEXC does not operate a US-licensed product, US IPs are blocked at signup, and the terms of service explicitly prohibit US persons. UK retail access is restricted under FCA rules for certain product categories. Canada has tightened access for crypto-asset platforms generally. Several other jurisdictions (Singapore retail, Hong Kong retail, Japan) have varying restrictions.

The platform’s geographic strength is in Southeast Asia, MENA (Middle East and North Africa), Russia, Turkey, and Latin America. Adoption in these markets has driven the bulk of MEXC’s user growth through 2024-2026. For users in these regions, MEXC operates as a primary or co-primary venue, often paired with a regional fiat on-ramp partner.

VPN warning: using a VPN to bypass the geo-block creates withdrawal risk. If MEXC later identifies the account as US-resident or as resident in another prohibited jurisdiction (through KYC, IP correlation, or partner-data signals), the platform can freeze withdrawals pending verification. The risk is most acute for US-resident accounts using a VPN, because the platform’s compliance posture treats US persons as a binary disqualification rather than a verification challenge. Do not use a VPN to access MEXC if you are US-resident.

For US-based traders the right answer remains a US-licensed venue: Kraken, Coinbase, or Gemini. For non-US users in restricted jurisdictions, verify availability directly on MEXC before depositing material capital.

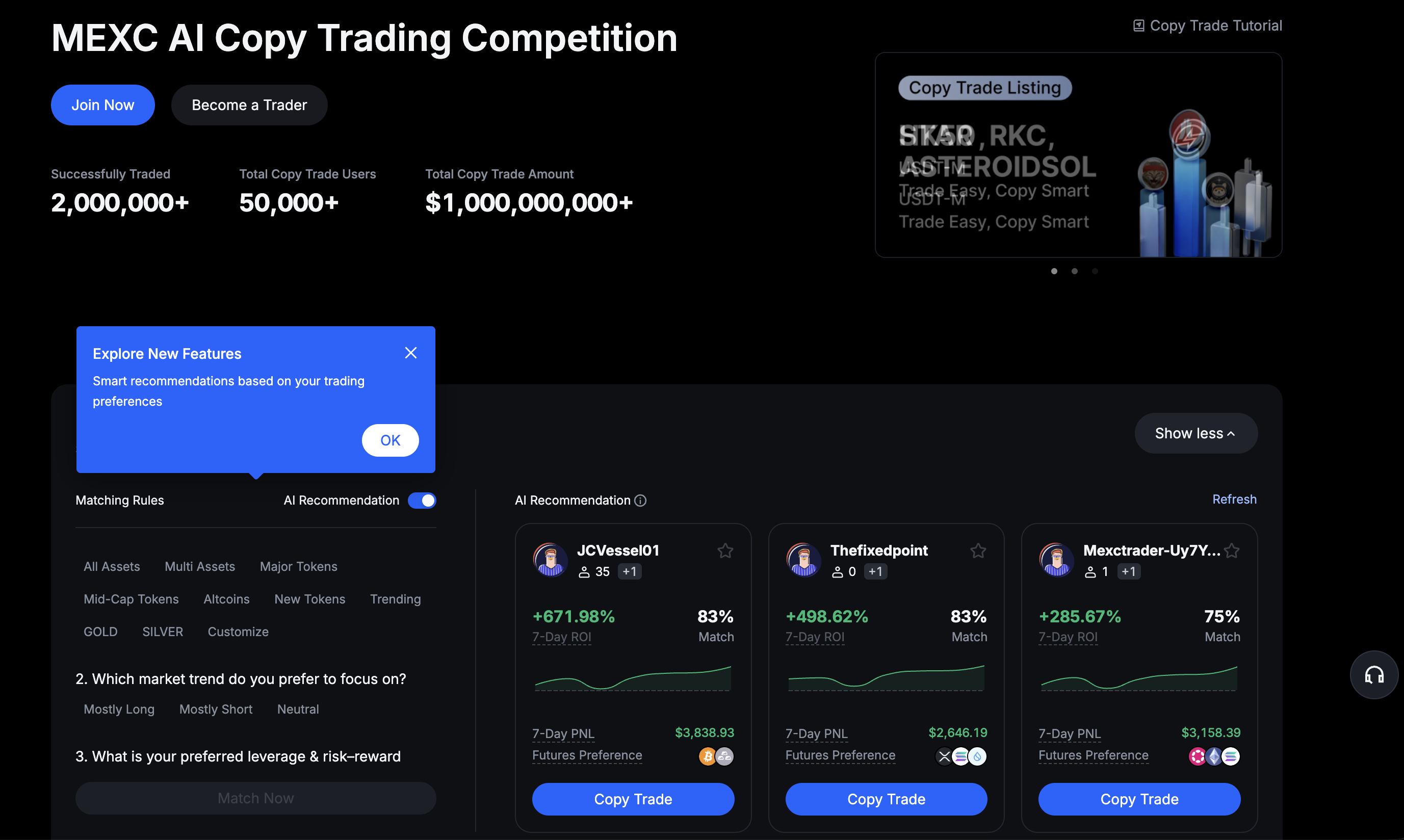

Copy trading

MEXC launched its copy trading product more recently than Bybit, BingX, or Bitget. The marketplace is functional and growing, but the lead-trader pool is shallower than the leading dedicated copy trading platforms. The product exposes filterable lead-trader metrics: 30-day PnL, win rate, follower count, AUM, average holding time, drawdown, and similar standard fields.

Lead-trader profit-share on MEXC is typically structured at 10-15 percent of follower net winning periods, which is in line with peer norms. Losing periods do not pay the lead trader anything but the follower still eats the full loss plus underlying trading fees on those positions. This is the standard copy trading model across CEXs; the implementation matters more than the headline split.

Tracking lead-trader counts across major CEX copy trading marketplaces through Q1 2026: BingX had roughly 50,000+ active lead traders, Bitget around 80,000+, Bybit around 15,000+, KuCoin around 5,000+, and MEXC around 3,000-4,000. MEXC’s pool is the smallest among the major venues with developed copy trading products, though growth velocity has been faster than KuCoin’s in the same window.

for users whose primary motivation is copy trading specifically, BingX and Bitget have deeper marketplaces with more aggressively curated lead-trader pools. For users who want copy trading available alongside MEXC’s altcoin breadth, aggressive fees, and futures depth, the product is functional. For pure copy-trading focus, see our BingX review for the strongest dedicated marketplace context.

The copy trading product on MEXC also has fewer altcoin-perpetual lead traders than Bitget despite MEXC’s broader altcoin coverage on spot. The mismatch is structural: MEXC’s altcoin-perpetual liquidity at the long tail is thinner than Bitget’s despite a wider listing, which constrains how much follower volume can be routed into smaller pairs without slippage problems.

A practical note on copy trading risk management: the average follower on any CEX copy trading marketplace loses money on a 12-month horizon, regardless of which platform. This is true on BingX, Bitget, Bybit, KuCoin, and MEXC alike. The high-PnL lead traders visible at the top of marketplace rankings are typically survivors of multi-month luck windows; reversion to mean tends to pull most lead traders into losing periods within 6-12 months of peak ranking. The realistic use case for copy trading is small allocations, diversified across multiple lead traders, with active monitoring of drawdown and position-sizing exposure. Treating copy trading as a passive yield product is the most common follower error and the one that produces the worst outcomes.

Security track record

MEXC’s security track record is clean on the most important measure: no major user-funds exploit comparable to Bybit’s 2025 incident, the 2019 Binance hack, or the 2014 Mt. Gox collapse. The platform has run continuous withdrawals across every meaningful market-stress event since 2018 (Terra collapse, FTX implosion, SVB stablecoin de-peg, 2024-2025 market volatility windows) without reported suspension at the platform level.

The trade-off is transparency. MEXC publishes proof of reserves but on a less rigorous cadence than Binance, Coinbase, or even peer mid-tier CEXs like OKX. The Merkle-tree attestation cadence has been described by independent observers (Chainalysis, Nansen, the proof-of-reserves auditor community) as less frequent and less granular than top-tier peers, with longer gaps between attestations and a smaller asset coverage than the most rigorously-attested platforms.

The transparency gap is the single biggest structural risk on MEXC relative to top-tier peers. A clean operating history is meaningful but does not provide forward-looking protection: an exchange can run cleanly for years and then surface a hidden liability under stress (the FTX failure mode). The mitigation is rigorous, frequent, third-party-audited proof of reserves, which Binance and Coinbase ship at higher quality than MEXC currently does. The implication is not that MEXC is dishonest; it is that the available evidence for verifying solvency is thinner than at the top tier, and users should weight that gap in their custody-allocation decisions.

Support quality during incident windows has been reported as below top-tier peers. User reports on social channels (Reddit, Twitter, dedicated community forums) consistently describe slower response times during high-volume events, less detailed root-cause explanations during outages, and longer resolution windows for individual-account issues like withdrawal delays or KYC review escalation. This is comparable to KuCoin and below Binance or Coinbase.

The forward-looking risk assessment: MEXC’s custodial-CEX risk shape is comparable to peers like KuCoin or Bitget, with the transparency gap as the meaningful negative versus the top tier. For long-term holdings the standard rule applies: keep on-platform only what you have actively allocated to open positions or short-term yield products; withdraw the rest to self-custody.

Two additional security considerations are worth flagging. First, account-level security on MEXC supports the standard set: password, two-factor authentication via authenticator app, anti-phishing code, withdrawal whitelist, and email confirmation for sensitive operations. Hardware-key two-factor (FIDO2 / WebAuthn) was added in 2024 and is the strongest available option; if your account holds any meaningful balance, enable it. Second, MEXC has been the target of phishing campaigns that mimic the platform’s login surface, which is common across major CEXs. Always verify the URL before logging in and bookmark the official login page rather than reaching it through search.

Comparison with Bybit, Binance, KuCoin

Direct comparisons across the major CEX peers, focused on where MEXC wins and loses.

MEXC vs Bybit

MEXC wins on altcoin breadth (2,800+ pairs versus roughly 400), on listing speed (often days to weeks faster), on default fee structure (0 percent maker on spot and futures versus 0.10 percent and 0.02 percent), and on no-KYC ceiling (still meaningful versus near-zero on Bybit post-2025).

Bybit wins on derivatives execution depth on top pairs, on options markets (BTC and ETH options with usable liquidity, which MEXC does not match), on copy trading marketplace maturity (15,000+ lead traders versus 3,000-4,000), on incident-response track record (the 2025 hack demonstrated capability MEXC has not been stress-tested on at the same scale), and on proof of reserves rigor.

Head-to-head verdict: MEXC for altcoin-heavy strategies with sensitivity to fees and no-KYC; Bybit for derivatives-heavy strategies with options exposure or active copy trading. Full Bybit context in our Bybit review.

MEXC vs Binance

MEXC wins on altcoin breadth (2,800+ versus 500), on listing speed (Binance’s review process is materially slower), on default fee structure on futures (0 percent maker versus 0.02 percent), and historically on no-KYC posture (Binance has tightened to near-zero for unverified accounts).

Binance wins on top-pair liquidity (deeper order books on BTC, ETH, SOL), on product surface breadth (Earn, Launchpad, NFT marketplace, P2P, fiat ramps), on proof of reserves rigor and transparency, on regulatory licensing footprint (more jurisdictions formally licensed), and on incident-response track record over a longer operating history.

Head-to-head verdict: MEXC as a secondary venue for altcoin breadth alongside Binance as a primary venue for top-pair execution and trust profile. The pattern most active retail traders settle into is multi-exchange use, not single-platform concentration.

MEXC vs KuCoin

MEXC wins on altcoin breadth (2,800+ versus 700), on default futures fee (0.02 percent taker versus 0.06 percent at KuCoin), and on no-KYC ceiling.

KuCoin wins on trading bots (KuCoin’s native bot stack is the most developed among CEX peers), on KCS daily yield (KCS pays a continuous daily platform-revenue share that MX does not match), and arguably on community-curated copy trading depth.

Head-to-head verdict: MEXC if altcoin breadth and aggressive fees dominate; KuCoin if trading bots and KCS-yield economics dominate. Full KuCoin context in our KuCoin review.

Who should use MEXC, and who should not

Across the platforms we test continuously, the MEXC user profile that produces the best outcomes is consistent. Three categories of trader benefit most.

Altcoin specialists. Users running early-listing strategies, capturing post-launch volatility on tokens before peer exchanges list and concentrate liquidity. The 2,800+ spot pair catalog and the listing-speed advantage are the structural moat here.

Fee-sensitive high-volume traders. Users running monthly volumes above $100K who care about the cumulative cost of trading fees. The 0 percent maker fee structure and the further VIP curve reductions produce meaningful real savings over a year of active trading.

Users in regions with KYC sensitivity. Users in jurisdictions where the no-KYC posture remains meaningful, who need a generous unverified ceiling for operational reasons. The current MEXC ceiling, while lower than historical, is still meaningfully higher than Binance, Bybit, or Coinbase.

The user profile MEXC does not serve well is also consistent. Four categories of trader should look elsewhere.

US-based traders. MEXC does not operate a US-licensed product. The right answer is Kraken, Coinbase, or Gemini.

Users prioritizing transparency. If proof of reserves rigor and corporate-disclosure quality are decision-driving factors, Binance or Coinbase is a better venue. The MEXC transparency gap is real even though the operating history is clean.

Derivatives specialists with options exposure. MEXC does not list deep options markets. Bybit or Deribit is the right venue for options-heavy strategies.

Users primarily focused on copy trading. BingX or Bitget have deeper marketplaces. MEXC’s copy trading product is functional but smaller. See our BingX review for context.

How to sign up

The signup flow is short. Email or wallet, optional referral code, and you are inside the platform with a tradable account before committing to verification.

- Use the signup link. Sign up at mexc.com/register. Use an email you control with a strong password. Enable hardware-key two-factor authentication immediately; platform-side exploits exist but user-side compromises are far more common.

- Decide on KYC strategy. Trade without verification if your withdrawal needs fit within the regional unverified ceiling; complete Primary KYC if you need higher limits, copy trading access, or fiat on-ramp paths. Standard verification (government ID, address proof) is typically minutes to a few hours for clean applications.

- Deposit USDT on Tron. Tron is the cheapest meaningful network. Confirm the network on both ends before sending. Wrong-network sends are the most common user-error fund loss.

- Test withdrawal early. Send a small amount back to self-custody. Verify the withdrawal path before scaling the balance. This is the single most important operational check on any new CEX.

- Start with spot before futures. Futures liquidation can wipe an account in minutes. MEXC’s 200x leverage on majors makes this risk acute. If you are new to perpetuals, paper-trade or use very small position sizes for a meaningful period before scaling.

- Consider MX if your volume justifies it. Otherwise skip the token and re-evaluate after a month of platform use. M-Day participation is the strongest reason to hold; the fee discount alone rarely justifies the price-risk exposure for users under $50K monthly volume.

Bottom line

In 2026, MEXC is the strongest altcoin-breadth centralized exchange for retail traders running early-listing strategies, fee-sensitive high-volume trading, or operations in regions where the no-KYC posture remains meaningful. The 2,800+ spot pair catalog, the 0 percent maker fee structure, and the M-Day airdrop mechanic are real structural advantages that no major peer matches at the same combination.

The 7.6 out of 10 score breaks down like this. Above KuCoin on listing speed and fee structure, comparable to Bitget in altcoin breadth and trader-pool depth, below Bybit on derivatives execution and copy trading maturity, below Binance on transparency and top-pair liquidity. The transparency gap and the support quality pull the score below the top-tier peer set. The clean operating history and the aggressive fee economics pull it above the second-tier venues.

For a retail trader running an altcoin-heavy strategy with attention to fees and willingness to accept higher long-tail listing risk, MEXC is a credible primary or co-primary venue in 2026. For US-based traders, derivatives specialists with options exposure, or users who prioritize transparency above fee economics, look elsewhere. The healthiest pattern most active retail traders settle into is multi-exchange use with MEXC as the altcoin-breadth and fee-aggressive node alongside a top-tier peer as the trust-and-liquidity anchor.

Open account: Register on MEXC. See the affiliate disclosure for full detail.

Read next

- Bybit review. Derivatives specialist with mature copy trading and options markets.

- KuCoin review. The sibling mid-tier CEX with KCS daily-yield economics.

- BingX review. The copy-trading-first alternative.

- Methodology. How we evaluate platforms.

- Risk disclaimer.

Frequently asked questions

Is MEXC safe to use in 2026?

Yes, with the standard centralized-exchange custodial risk that applies to every CEX. MEXC has no public record of a major user-funds exploit comparable to the 2025 Bybit incident or the 2019 Binance hack, and the platform has run continuous withdrawals through every market-stress event since 2018. The trade-off is transparency: MEXC publishes proof of reserves but on a less rigorous cadence than Binance or Coinbase, the corporate structure is opaque, and support quality during incident windows is below the top tier. Treat MEXC as a trading venue, not a long-term storage solution, and the risk shape is comparable to peers.

What are MEXC's trading fees?

Spot fees are 0 percent maker and 0.1 percent taker at default tier, which is already aggressive compared to most peers. Many promotional pairs run at 0 percent both sides on a rotating basis. Perpetual futures cost 0 percent maker and 0.02 percent taker at default tier, the lowest headline futures fee among major CEXs. Activating the MX token fee discount lowers eligible trading fees by 20 percent. VIP tiers scale further based on 30-day rolling volume. Withdrawal fees depend on the network: USDT on Tron is typically 1 USDT flat, the cheapest meaningful path.

Can I use MEXC without KYC in 2026?

Partially, and the rules tightened materially through 2025. Historically MEXC allowed unverified accounts to withdraw up to roughly 10 BTC per day, which made it the most generous no-KYC posture among large CEXs. In 2026 the unverified ceiling is lower (commonly cited at around 30 BTC equivalent in lifetime withdrawals before mandatory verification triggers), with regional variations. Trading itself still works without KYC for spot and futures in most jurisdictions, but withdrawal limits, copy trading, and some launchpad products now require Primary KYC. Verify the current ceiling in your region before depositing material capital.

Does MEXC have copy trading?

Yes. MEXC launched its copy trading product more recently than Bybit, BingX, or Bitget and the marketplace is smaller. The platform exposes filterable lead-trader metrics (PnL, win rate, follower count, AUM, drawdown) comparable to peer interfaces. Lead-trader profit-share is typically 10-15 percent on net winning periods. For users whose primary motivation is copy trading specifically, BingX and Bitget still have deeper marketplaces. For users who want copy trading available alongside MEXC's altcoin breadth and aggressive listings, the product is functional and growing.

Can US users use MEXC in 2026?

No. MEXC does not serve US users and does not operate a US-licensed product. The platform's terms of service prohibit US persons and US IPs are blocked at signup. Using a VPN to bypass the geo-block violates the terms of service and creates withdrawal risk if the platform later identifies the account as US-resident. For US-based traders, the right answer is a US-licensed venue: Kraken, Coinbase, or Gemini. Outside the US, MEXC is broadly available, with strong adoption in Southeast Asia, MENA, Russia, and Turkey.

What is MX token and is it worth holding?

MX is MEXC's native utility token. Holding MX activates a 20 percent trading fee discount and grants access to M-Day, the platform's recurring airdrop event where MX holders share allocations of newly listed tokens. M-Day historically distributes a portion of new-listing supply pro rata to MX positions held during a snapshot window, which has produced meaningful realized yield for active participants. Unlike KuCoin's KCS, MX does not pay a continuous daily revenue-share bonus. The value proposition combines the fee discount plus M-Day airdrop access. For active traders running monthly volume above $50K and willing to participate in M-Day cycles, MX can make sense.

How does MEXC compare to Bybit, Binance, and KuCoin?

Versus Bybit: MEXC has materially more altcoin pairs (roughly 2,800 vs Bybit's 400) and a more generous no-KYC posture; Bybit has tighter derivatives execution, options markets, and a more mature copy trading marketplace. Versus Binance: Binance is the broader and more transparent platform with deeper top-pair liquidity; MEXC wins on listing speed and altcoin breadth. Versus KuCoin: MEXC has more pairs and lower futures fees; KuCoin has stronger trading bots and the KCS daily-yield mechanism. Head-to-head detail in our [KuCoin review](/blog/kucoin-review/) and [Bybit review](/blog/bybit-review/).

What are the realistic risks of using MEXC?

Three risks matter most. First, listing-speed risk: MEXC's edge is listing new tokens faster than peers, which means a higher share of the long tail is high-rug-risk or low-liquidity. Second, transparency risk: MEXC publishes proof of reserves less rigorously than Binance and Coinbase, and the corporate structure is more opaque. Third, support risk: incident-window support quality has been reported as below top-tier peers, with delayed responses during high-volume events. None of these are exit-scam signals, but they are real operational considerations. Standard CEX rules apply: trade on platform, custody off platform.

#MEXC#exchange review#no-KYC#altcoins#MX token#copy trading#futures

Discussion

Loading comments…