Score: 8.4 / 10 · Good for: no-KYC perpetuals, self-custody traders, order book quality on top pairs, HYPE token alignment, lower fees at retail volume · Watch out: smart-contract and bridge risk, no fiat on-ramp, US frontend block, smaller asset list, no spot for most assets, total wallet-loss responsibility · Updated: May 2026

Hyperliquid is a perpetual-futures decentralized exchange built on its own purpose-built Layer 1 blockchain, launched in 2023 by Jeffrey Yan and the developer known as iliensinc with a singular product focus: a real on-chain central limit order book that competes with centralized venues on execution quality. The platform’s growth trajectory through 2024 and 2025 (culminating in the November 2024 HYPE token genesis airdrop, one of the largest community distributions in crypto history) pushed it into the top 10 perpetual-futures venues globally by volume, including against the major CEXs. This piece walks through what actually matters before you connect a wallet: the HyperBFT consensus and order book design, the HYPE token mechanics and TGE distribution, fees with volume and staking discounts, HLP vault behavior, the KYC story and US restrictions, the security trade-offs of a non-custodial venue, and where Hyperliquid fits in a multi-venue stack. We score every platform on the same methodology and affiliate considerations do not move the rankings.

Not financial advice. Crypto trading is high risk. Self-custody on Hyperliquid means user funds sit in a wallet under your sole control: there is no support desk that can recover a lost seed phrase, reverse a wrong-address withdrawal, or restore an account after a wallet compromise. Smart-contract risk on the Arbitrum bridge is real and not zero. Derivatives with leverage can wipe an account in minutes. Verify what is legal in your jurisdiction before connecting a wallet. Read the risk disclaimer.

What is Hyperliquid

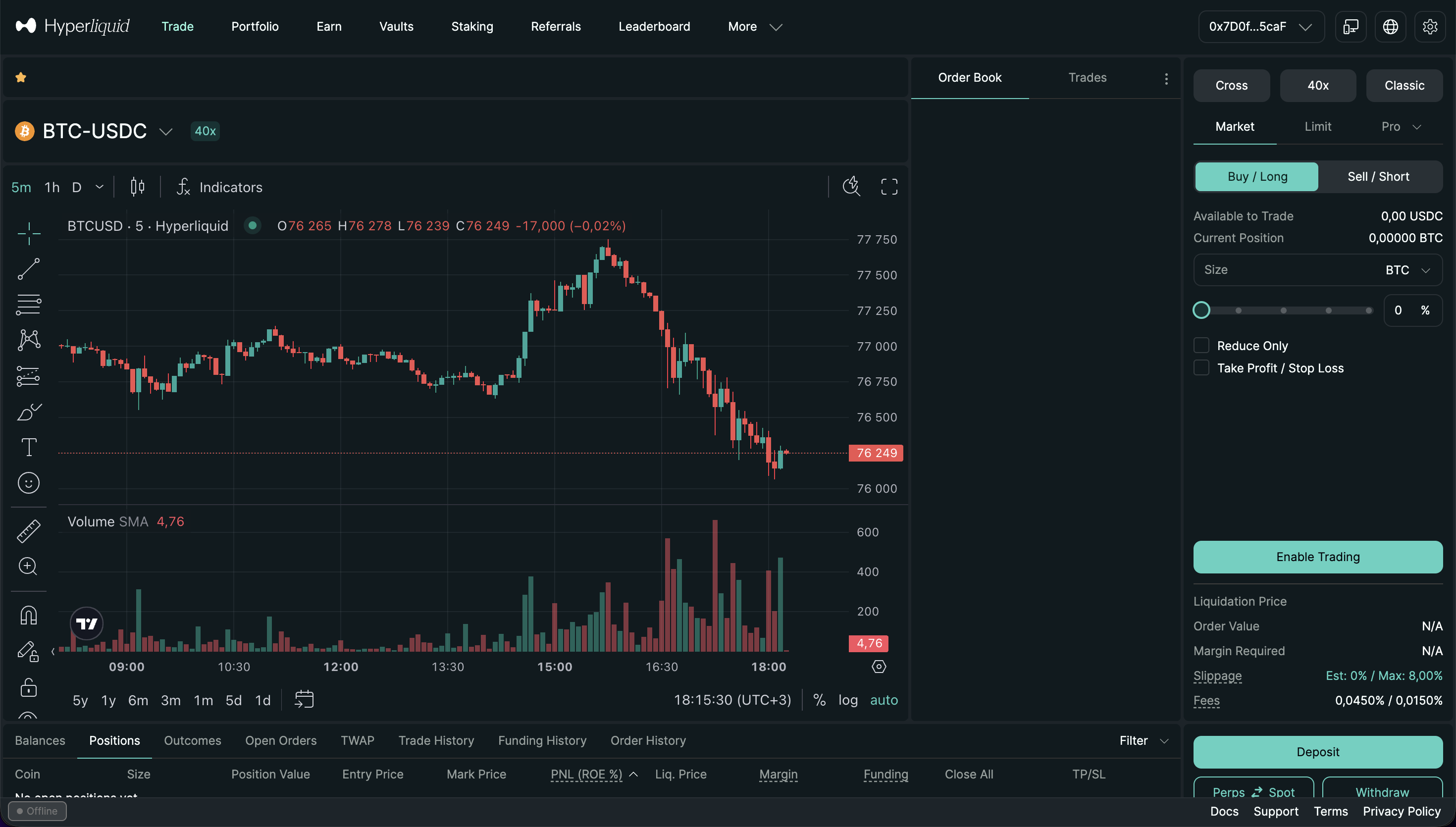

Hyperliquid launched its mainnet in 2023 with a deliberately narrow scope: build the highest-quality on-chain perpetual-futures order book in the industry and let the product define the platform. The founders, Jeffrey Yan and the pseudonymous developer known as iliensinc, came out of a quantitative-trading background and the design choices reflect that origin. The order book is a real CLOB (central limit order book), not an automated market maker. Trades match through price-time priority. Funding rates clear continuously. The matching engine lives in consensus rather than in a smart contract, which is the architectural decision that makes the rest of the design viable.

The platform runs on its own Layer 1 blockchain rather than as a smart contract deployed on Ethereum, Arbitrum, or a similar general-purpose chain. The HyperBFT consensus algorithm is a Byzantine Fault Tolerant variant tuned for the latency profile that order book matching requires. Block times target sub-second finality. Order placement, cancellation, and matching are first-class operations in the consensus protocol, not generic smart-contract calls. The result is that interacting with Hyperliquid feels closer to a centralized matching engine than to a typical DEX. There are no gas fees on individual order operations. There is no MEV extraction on the order book side because the matching is deterministic and ordered through consensus.

The trade-off of this architecture is that Hyperliquid does not get composability with the broader Ethereum DeFi stack the way a smart-contract DEX would. Bridges in and out are explicit and run through Arbitrum, which serves as the canonical deposit and withdrawal route for USDC. This is a deliberate design choice: the platform optimizes for execution quality over interoperability, on the bet that the trader segment cares more about a tight book than about flash-loan composability. Through 2025 the bet looks correct.

Operationally, Hyperliquid Labs (the team behind the protocol) maintains a low public profile relative to the platform’s volume share. There is no headquarters in the traditional CEX sense, no corporate registration in a single major jurisdiction that gates the protocol. Governance is on-chain through HYPE staking and validator set decisions. The team has shipped consistently and avoided the public missteps that defined some 2023-2024 DeFi protocols, but the lower transparency floor of pseudonymous-cofounder operations is part of the risk shape and worth naming explicitly.

The product identity in 2026 rests on four pillars. First, order book quality: spreads and depth on BTC and ETH perpetuals are now competitive with Bybit and Binance at retail size. Second, no-KYC access: the protocol is permissionless, with frontend geo-blocking that is meaningfully softer than the compliance posture of the major CEXs. Third, the HYPE token: the November 2024 TGE distributed approximately 28 percent of supply directly to community users, and the token now functions as the fee-discount and validator-staking asset. Fourth, the HLP vault: a passive market-making vault that turned into one of the most-watched yield products in DeFi through 2025.

The HYPE token and 2024 TGE

The HYPE token generation event on November 29, 2024 became a reference point for community-first crypto distributions. The genesis allocation distributed approximately 28 percent of total supply (around 310 million HYPE out of a 1 billion maximum) directly to a snapshot of early users and traders, with no vesting on the airdrop tranche. Snapshot eligibility was based on documented platform activity through 2024: trading volume, vault participation, points accumulated through the points program that ran in the months before the TGE.

The distribution model broke from the typical 2021-2023 pattern. VC-backed launches of comparable scale usually allocated 30-40 percent of supply to private investors with multi-year vesting cliffs, 15-20 percent to team and advisors, and a residual 10-15 percent to community through capped airdrops or liquidity programs. Hyperliquid inverted this. The team, treasury, and ecosystem allocations were smaller in relative terms. There was no VC seed or Series A round preceding the TGE. The community share was both larger as a percentage and unlocked, which created the price discovery dynamic that followed.

In the weeks after the TGE, HYPE traded from initial price discovery in the low single digits to mid-double digits by early 2025 as the airdrop recipients sorted into long-term holders and sellers. The fully-diluted valuation cleared $20 billion at the early-2025 peak, which placed HYPE in the top tier of crypto market capitalizations within months of launch. This is unusual: most large-airdrop token launches see sustained downward price pressure as recipients exit. HYPE’s relative resilience is generally attributed to the fee-discount staking mechanic, the ongoing protocol-level buyback funded by trading fee revenue, and the platform’s trading volume growth through the same period.

The token has three mechanics that matter for traders, not just speculators. First, fee discount on staking: locking HYPE in the staking module reduces taker fees through a separate discount layer that stacks with volume-based VIP tiers. Second, validator staking: HYPE is the security asset for the Hyperliquid L1, with validators required to bond meaningful HYPE balances and inflation-style rewards paying back to stakers. Third, governance: protocol parameter changes and asset listings route through HYPE holder governance, with the validator set retaining final ratification authority. The governance throughput is intentionally low; this is a feature, not a bug.

For users evaluating HYPE as a portfolio position rather than a fee-discount tool, the standard framing applies. The token is concentrated in a smaller number of large holders than its airdrop origin would suggest, because secondary-market accumulation through 2025 consolidated supply among funds and high-volume traders. The fee-buyback mechanic creates a real cash flow that backs the token economically, but the discount rate one applies to that cash flow is debatable and the token trades at multiples that imply continued aggressive volume growth. Treat HYPE as a high-beta exposure to Hyperliquid platform success, not as a stable yield asset.

Markets and asset coverage

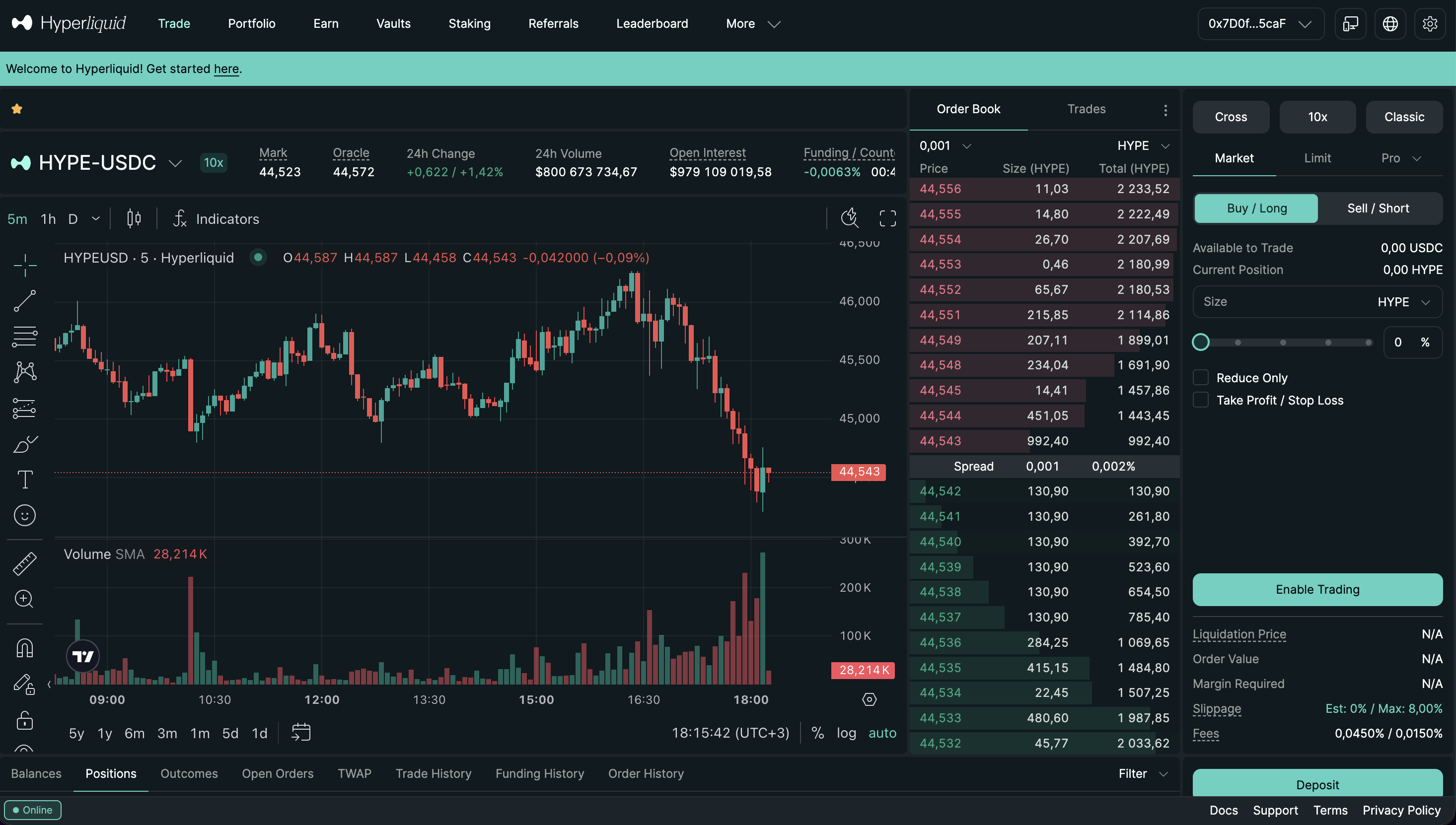

Hyperliquid lists approximately 150 to 200 perpetual-futures pairs as of 2026, all USD-margined through USDC collateral. The list skews toward the most liquid crypto assets: BTC, ETH, SOL, and the top 100 by market capitalization make up the core liquidity, with a long tail of smaller pairs that have meaningfully thinner books. Leverage caps differ by pair: BTC and ETH allow up to 50x, mid-cap pairs typically cap at 20x to 25x, and smaller pairs are restricted to 5x or 10x for risk-management reasons.

There is no spot market for the majority of assets. Hyperliquid is a perpetuals-focused venue and the trading workflow assumes USDC deposit, then perpetual exposure rather than asset-level holdings. A small spot market exists for select assets including HYPE itself and a limited basket of high-volume tokens, but it is not the primary product surface. For traders who want spot exposure to a token they trade on Hyperliquid, the typical pattern is to use the perpetual for active trading and execute spot purchases elsewhere (a major CEX or a different DEX). This split is a real ergonomic friction relative to a CEX that bundles spot and futures.

Liquidity quality on top pairs is now genuinely competitive with the leading CEXs. BTC-USD perpetual depth at the top of book on Hyperliquid through 2025-2026 routinely matched or exceeded Bybit’s at comparable price points, and spreads on top pairs tightened to one or two basis points during high-volume periods. This is a substantive change from the 2023-2024 state of the platform when liquidity was respectable but clearly behind the CEX tier. The combination of the HLP vault providing baseline market making, the JIT auction mechanism for incentivized maker fills, and organic professional market maker participation post-TGE pushed top-pair quality into a competitive range.

The long-tail trade-off remains. Mid-cap altcoin perpetuals on Hyperliquid have thinner books than the same pairs on Binance or Bybit. Slippage on a $50K order in a top-50-but-not-top-10 pair can be materially worse than the CEX equivalent. For traders concentrating in the most-liquid pairs (BTC, ETH, SOL, the top 10 to 20), Hyperliquid is now a credible execution venue. For traders running long-tail altcoin strategies with size, the CEX route still typically wins on depth.

The asset listing process favors quality over breadth. New pair listings go through governance review and are gated by liquidity and oracle-quality requirements. The result is a shorter list than Binance Futures (which lists 300+ perpetuals) or Bybit (200+), but with less listing-quality variance. This is consistent with the platform’s broader stance: optimize the high-value subset rather than chase coverage.

Order book architecture

The defining technical decision in Hyperliquid is the on-chain central limit order book, hosted directly in consensus rather than as a smart-contract overlay. Every order placement, cancellation, modification, and match is a first-class operation in the HyperBFT consensus protocol. There are no AMM curves. There is no liquidity pool slippage formula. Orders rest on a book with price-time priority, exactly as on a centralized exchange, with the matching engine running as part of validator consensus.

Comparing this to other on-chain order book attempts is instructive. dYdX v3 ran an order book but kept matching off-chain on a centralized sequencer that posted results to StarkEx for settlement. The v3 model was fast but the matching itself was not decentralized in a meaningful sense; the sequencer was a single operator. dYdX v4 (launched late 2023) migrated to a Cosmos-based appchain with validator-run matching, which is architecturally closer to Hyperliquid but with different consensus-level optimizations. Hyperliquid’s HyperBFT design pushes the order book deeper into the consensus protocol, batching order book state transitions into consensus blocks directly rather than treating orders as application-layer messages.

Just-in-time (JIT) auctions are the second key mechanism. When a taker order arrives at the book, a brief auction window allows market makers to compete for the fill. This routes liquidity provision to the most-aggressive maker for that specific moment, which improves execution quality for the taker and creates an explicit incentive structure for professional market making. The JIT mechanism is layered on top of the standard CLOB rather than replacing it; resting limit orders still fill in price-time priority outside the auction window.

Pre-confirmation policy (PCP) is the third architectural element worth understanding. The Hyperliquid L1 surfaces pre-confirmations to the frontend within the consensus round-trip, meaning users see order placement and match confirmations on a sub-second cadence that approximates the responsiveness of a centralized matching engine. This is not the same as final settlement (which clears at block finality), but for the purposes of active trading the experiential gap between Hyperliquid and a CEX matching engine has effectively closed on top pairs.

The trade-off of pushing the order book this deep into consensus is that protocol-level changes (new order types, new market mechanics, new asset classes) require coordinated validator-set upgrades rather than smart-contract redeploys. This makes Hyperliquid harder to iterate on at the application layer compared to a smart-contract DEX. The team has shipped substantive upgrades through the 2024-2026 window, but the cadence is closer to a centralized-exchange release schedule than to a DeFi-native protocol with permissionless deployment.

Fee structure

At default tier, Hyperliquid charges approximately 0.025 percent taker on top perpetual pairs and pays a 0.005 percent maker rebate. The maker rebate is unusual for a DEX and is funded by the same revenue pool that powers the HYPE buyback; the structure is designed to attract resting liquidity to the book. Volume-based VIP tiers scale the taker fee down meaningfully and the rebate can scale up at the highest tiers. Staking HYPE adds a separate discount layer that stacks with the volume-based tier.

| Tier | Maker / taker (top pairs) | 14-day volume threshold |

|---|---|---|

| Default | -0.005% rebate / 0.025% | none |

| Tier 1 | -0.005% rebate / 0.022% | $5M |

| Tier 2 | -0.010% rebate / 0.019% | $25M |

| Tier 3 | -0.015% rebate / 0.016% | $100M |

| Tier 4 | -0.020% rebate / 0.013% | $500M |

Staking HYPE adds a discount on top of these tiers. At meaningful HYPE-staked balances the taker fee on top pairs can drop to single-digit basis points, which is competitive with VIP 3+ rates at Bybit or Binance for substantially lower volume thresholds. The cumulative discount math favors active traders who would hold HYPE as a position anyway; for users who are not HYPE holders, the default volume tier alone is already competitive with mid-tier CEX rates.

Across the 2025 trading year, the median effective taker fee on Hyperliquid (factoring in volume tier distribution and staking) settled at approximately 0.018 to 0.020 percent for active retail traders, which is roughly 10 to 15 percent below the equivalent BIT-discounted Bybit rate at comparable volume, and meaningfully below default Binance Futures pricing.

There are no gas fees for placing orders on the Hyperliquid L1. The chain is purpose-built and order operations are free at the user-experience level (the validator set is compensated through fee revenue, not per-transaction gas). This is a real ergonomic differentiator versus running an order book on a general-purpose chain where every order, cancel, and amend costs gas. For high-frequency or active retail traders this changes the cost structure of basic order management.

Bridge deposit and withdrawal fees are separate. Deposits from Arbitrum incur standard Arbitrum L2 gas, typically a few cents to a dollar depending on network conditions. Withdrawals incur both L2 gas and a small protocol fee on the withdrawal side, generally in the low-single-digit USDC range. Always confirm the network and address on both ends before sending. Wrong-network transfers on bridge withdrawals are recoverable in some cases but the recovery path is technical and not guaranteed.

Funding rate is separate from trading fees. Perpetual contracts pay or receive funding on a continuous basis (the rate clears every block rather than at fixed 8-hour intervals as on most CEXs), which smooths the funding profile and reduces the gaming around scheduled funding times. For sustained-bias positions, the continuous funding mechanic generally reduces total funding cost variance relative to the 8-hour CEX cadence, though the long-run average funding rate on a heavily one-sided pair will still be material.

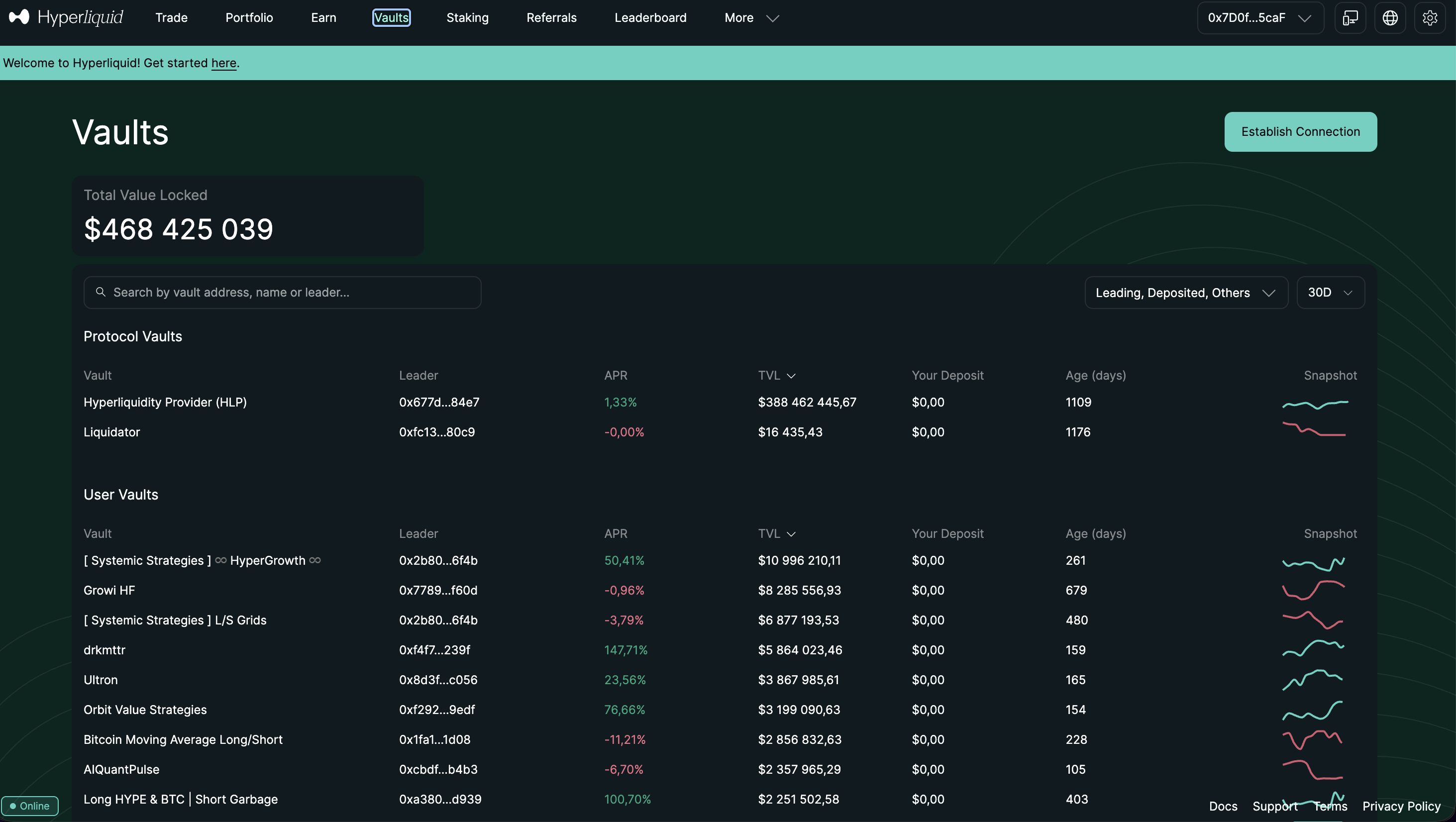

HLP and trading vaults

The Hyperliquidity Provider (HLP) vault is one of the most distinctive products on the platform. It is a passive vault that accepts USDC deposits and deploys them as market-making capital inside the Hyperliquid order book. Vault depositors earn a share of the market-making PnL pro-rata to their deposit. The vault is operated programmatically through the protocol; there is no external manager taking fees off the top. The mechanism is designed to give passive capital exposure to professional-style market-making returns without requiring the depositor to run any infrastructure.

HLP returns through the 2024-2025 window settled in a range that varies meaningfully with market conditions. During high-volume, high-volatility periods (notably the post-TGE window in late 2024 and the Q1 2025 rally) HLP delivered annualized returns in the 20 to 25 percent range. During quieter market regimes (parts of mid-2025) returns compressed to the high single digits or low double digits annualized. The historical return profile is real but not guaranteed; HLP can and has had drawdown periods when market-making positions sit on the wrong side of a sharp move.

The HLP vault is structurally short volatility and short the smart-trader segment of taker flow. When the trader population is collectively wrong (the typical pattern, given retail trader behavior), the vault profits. When a sharp directional move catches the vault wrong-footed (the tail event), the vault takes losses that flow back to depositors. The 2025 drawdown periods on HLP were modest in absolute terms (single-digit-percent drawdowns rather than the 20 to 30 percent drawdowns that some 2021-2022 yield products experienced), but they are real and the marketing framing of HLP as “passive yield” understates the risk shape. Treat HLP as a market-making strategy with retail access, not as a stablecoin yield product.

User-created vaults are a separate product alongside HLP. The vault module allows any user to create a vault, deposit capital, run a discretionary or systematic strategy through the standard trading API, and accept third-party deposits. Vault creators take a performance fee (typically 10 to 20 percent of net profits, configurable per vault). The model is structurally similar to copy trading on a CEX, but the implementation is on-chain and the capital flows are transparent. The user-vault product surface is real but the depth and quality of available vaults varies; due-diligence rigor on a vault creator is no different from due-diligence rigor on a copy-trading lead trader.

The vault economics are worth understanding before depositing. HLP is non-redeemable on demand: deposits enter the vault and can be withdrawn only after a multi-day lockup period (currently around 4 days), which exists to prevent users from gaming the vault around expected volatility events. User-created vaults have configurable lockup periods set by the creator. For capital that needs immediate liquidity, the vault products are not the right home. For capital with a multi-week or multi-month time horizon, the risk-adjusted returns through 2024-2025 have been competitive with most DeFi yield options.

KYC and country availability

Hyperliquid does not require KYC at the protocol level. Account creation is wallet connection. There is no email signup, no government ID upload, no liveness selfie, no source-of-funds questionnaire. This is the structural difference between a non-custodial DEX and a centralized exchange: the protocol has no custody of user funds, and therefore has no regulatory hook that compels customer identification. The wallet is the account.

The frontend at app.hyperliquid.xyz applies geo-blocking based on IP address. US IPs are blocked at the frontend layer. Several other jurisdictions also see some level of frontend restriction depending on the legal environment for derivatives in those regions. This is a frontend-only restriction; the on-chain protocol is permissionless and can be accessed through alternative frontends, direct contract interaction, or other interfaces that the protocol itself does not control.

The VPN reality on Hyperliquid is what users actually do, and it is worth being honest about it. Many users in geo-blocked jurisdictions access the platform through commercial VPNs and use it without further friction; the protocol does not check residency at any deeper layer. We do not advise this. The decision to access an offshore non-licensed venue from a restricted jurisdiction is a personal compliance choice that carries the same regulatory consideration as accessing any other geo-restricted financial product. The platform terms of service prohibit it. Legal exposure depends on jurisdiction, account scale, and enforcement posture in the user’s country.

For US-based traders looking for a regulated derivatives path in 2026, the answer is not Hyperliquid. CME crypto futures, regulated US options venues, or US-licensed spot exchanges with associated derivatives products are the correct path. The privacy and self-custody benefits of Hyperliquid do not offset the regulatory exposure for a US-resident user accessing an explicitly geo-blocked venue. For users in jurisdictions where Hyperliquid is available without restriction (most of Asia, Latin America, parts of Europe, the Middle East), the no-KYC posture is one of the platform’s strongest features.

The privacy framing matters beyond the regulatory question. On a CEX with full KYC, the platform holds a complete record of the user’s identity, trading activity, and balance history, which becomes a target for breach (every CEX breach in the 2018-2025 window leaked some level of customer PII) and a compliance dataset that can be queried by regulators, tax authorities, and law enforcement. On a non-KYC DEX, the on-chain footprint is public but is not directly tied to off-chain identity; this is a different privacy profile, not a higher one, and traders should understand the distinction before treating no-KYC as equivalent to privacy. See our best no-KYC crypto exchanges 2026 coverage for the broader landscape.

Security and decentralization trade-offs

Hyperliquid’s security model is meaningfully different from a CEX’s, and the differences cut in both directions. The headline benefit is non-custodial: user funds sit in self-controlled wallets rather than on the platform’s balance sheet, which removes the kind of custody-failure scenario that defined FTX in 2022 or the 2025 Bybit exploit. There is no analog to a hot-wallet drain on Hyperliquid in the same sense, because the protocol does not aggregate user funds into a wallet that can be drained.

The risks shift to a different set of failure modes. First, the validator set: Hyperliquid’s L1 is secured by a validator network that runs HyperBFT consensus and stakes HYPE as security collateral. The validator set is smaller than Ethereum’s (low double digits as of 2026 with planned expansion), which means consensus is more centralized in the literal head-count sense than a major L1 like Ethereum or Solana. The team has been clear that validator decentralization is a multi-year roadmap rather than a launch-state property, and the current configuration includes both team-affiliated and independent validators. The level of validator centralization is comparable to other newer appchains (dYdX v4, certain Cosmos chains) but worse than mature L1s.

Second, the Arbitrum bridge. The canonical deposit and withdrawal route for USDC runs through a bridge contract on Arbitrum. The bridge is the single largest smart-contract risk surface in the Hyperliquid security model. It has been audited by reputable firms and has operated without exploit through the 2024-2026 window, but bridge contracts have been the most frequent target of major DeFi exploits historically (the Ronin, Wormhole, and Nomad exploits in the 2022 window collectively drained more than $1 billion through bridge contract failures). A successful exploit on the Hyperliquid Arbitrum bridge would be the catastrophic event for the platform. The risk is documented, audited, and quantitatively small but not zero.

Third, oracle and sequencer risk. The Hyperliquid L1 uses oracle inputs for funding rate calculation and liquidation pricing. Oracle manipulation has been the vector for several DeFi exploits in adjacent protocols. The team has implemented multi-source oracle aggregation and sequencer-level redundancy, but the failure mode exists. Sequencer downtime (the validator set being unable to reach consensus due to a network event) would temporarily halt the platform; this is a documented risk shared by every newer appchain.

The 2024-2025 operational track record on Hyperliquid has been clean. No major exploit. No platform-side fund loss. No multi-day downtime event. This is a meaningful data point but it is also a short data window relative to Bybit’s eight-year operational history or Binance’s even longer track record. A platform’s first major stress event is informative in a way that uneventful operating periods are not. Hyperliquid has not yet had its FTX moment, its 2025-Bybit-exploit moment, or its bridge-exploit moment, and the absence of those events should be weighted as positive evidence but not as proof of long-run resilience. The institutional risk-management practice of capping exposure to any single venue applies to Hyperliquid as much as to any CEX.

The mitigation framing for individual users is straightforward. Keep on the platform only what you have actively allocated to open positions or short-term vault deposits. Use a dedicated wallet for Hyperliquid activity, not the same wallet that holds long-term cold storage. Bridge in only what is needed for the trading window. Bridge out promptly after closing positions. The security model assumes user-side discipline on wallet hygiene; the protocol cannot enforce it.

Comparison with Bybit, Binance, dYdX

Hyperliquid sits in a specific position in the perpetuals-venue landscape, and the comparison set is informative. Against the major CEXs (Bybit, Binance, OKX), Hyperliquid trades scale and asset breadth for self-custody and no-KYC access. Against the other major perp DEXs (dYdX, GMX, others), Hyperliquid trades smart-contract composability for order book quality and a dedicated L1 architecture.

Versus Bybit, the trade-off is clearest. Bybit wins on asset breadth (spot markets, options markets, structured products), fiat on-ramp (direct fiat-to-crypto deposits in supported regions), and the depth of long-tail altcoin liquidity. Hyperliquid wins on self-custody, no KYC, lower fees at retail volume, and a more aligned token model through HYPE. On top-pair execution quality, the two are now genuinely competitive; this is a recent development driven by Hyperliquid’s 2024-2025 liquidity growth post-TGE. For a trader running futures-heavy strategies on the top 10 pairs with no need for spot or options exposure, Hyperliquid is now a credible alternative to a Bybit-primary stack. See our full Bybit review for the CEX counterpart detail.

Versus Binance, the scale gap is wider but the directional trade-off is the same. Binance offers more pairs, deeper long-tail liquidity, a broader product surface (spot, futures, options, Earn, P2P, Card, Launchpad, structured products), and direct fiat on-ramp in most regions. Hyperliquid offers the same self-custody and no-KYC benefits as it does versus Bybit, with the same competitive top-pair execution. For retail traders whose primary need is liquid futures on the top pairs without KYC, Hyperliquid; for traders needing the full Binance product surface and scale, Binance.

Versus dYdX, the comparison is between two of the leading on-chain order book perp DEXs and the differences are more architectural than directional. dYdX v4 runs on its own Cosmos-based appchain with validator-run matching. Hyperliquid runs on HyperBFT with a deeper consensus-level integration of the order book. dYdX has a longer operating history (v3 launched 2021) but a more disruptive architecture migration in late 2023. Hyperliquid has stronger 2024-2026 momentum in volume, liquidity, and token economics. The HYPE TGE distribution and price action through 2025 pulled significant trader and liquidity provider attention to Hyperliquid that previously sat at dYdX. As of 2026 Hyperliquid leads dYdX in most perpetuals volume metrics, though dYdX retains a meaningful user base and product surface.

Versus GMX and the AMM-style perp DEX category, the comparison is structurally different. GMX and similar protocols use a pooled liquidity model where takers trade against a vault, rather than against resting limit orders. The model is simpler from a liquidity-provider perspective and has its own merits, but execution quality at scale is not competitive with a real order book. For traders prioritizing execution, the order book DEXs (Hyperliquid, dYdX) are the right comparison set; for traders prioritizing simpler LP economics or smaller-position-size convenience, the AMM-style perps are a different product.

The summary positioning is: Hyperliquid is now the leading non-custodial perp DEX by most volume metrics, and the leading no-KYC alternative to the major CEXs for futures-focused traders. The asset list is smaller, the on-ramp is harder, and the security history is shorter. The trade-offs are real in both directions, and the right venue depends on the trader’s specific workflow and constraints.

Who should use Hyperliquid (and who should NOT)

Hyperliquid fits a specific trader profile in 2026 and fails specific others. The fit cases first.

The platform is a credible primary venue for traders running futures-heavy strategies focused on the top 20 most-liquid perpetual pairs, who prioritize self-custody and privacy, who hold or can hold a crypto-native wallet, and who have monthly trading volume in the meaningful retail range (above approximately $50K). For this profile, the no-KYC access, the competitive order book quality, the HLP and vault product surface, and the HYPE-aligned economics all add up to a stronger value proposition than the CEX alternatives. Sophisticated retail derivatives traders coming from a multi-CEX background often add Hyperliquid as a primary venue alongside one or two CEXs rather than fully replacing the CEX stack.

The platform is a strong secondary venue for traders who want a self-custody perp DEX in their stack for specific use cases: privacy-sensitive positions, off-the-record speculative trades, or exposure to assets that have not yet listed on the user’s primary CEX. Even users whose primary trading venue is a CEX often maintain a Hyperliquid account for these flexibility cases.

The fail cases are clear. Beginners new to crypto trading should not start on Hyperliquid. The wallet-native workflow, the seed phrase responsibility, the bridge mechanics, and the perpetuals-only product surface create a steep learning curve that compounds with the standard derivatives learning curve. A first-time trader is much better served by a major CEX with paper-trading features, a fiat on-ramp, and a support desk; once core trading workflow is established, Hyperliquid can be added to the stack.

Users dependent on fiat on-ramps should not use Hyperliquid as a primary venue. The platform does not offer direct fiat-to-crypto conversion. The deposit workflow requires already-held USDC or USD-pegged stablecoin on Arbitrum, which means the user must onboard fiat through a CEX or an on-ramp provider, then bridge. For users whose typical workflow involves fiat deposits and withdrawals, Hyperliquid adds a meaningful friction step that a CEX does not impose.

Users running very small position sizes face an unfavorable cost structure. The bridge gas plus protocol fee plus normal trading fees mean that round-trip costs on a $100 position can be a meaningful share of the position value. For traders whose typical position size is below approximately $1,000, the cost economics tilt unfavorably toward Hyperliquid relative to a CEX with no bridge cost. The platform is built for meaningful retail size and above.

Users in jurisdictions where the platform is geo-blocked, who are unwilling to use VPN access, should not use Hyperliquid. The cleanest path for restricted-jurisdiction users is a locally-licensed venue, even at the cost of higher fees or KYC requirements. We do not advise VPN access to geo-blocked venues as a default workflow.

How to use Hyperliquid

The end-to-end deposit and trading flow has four primary steps. The platform assumes baseline familiarity with crypto wallets; if any of the steps below are unfamiliar, gain wallet-level fluency on a smaller dollar amount before scaling capital.

-

Set up a crypto wallet. MetaMask, Rabby, Frame, or another EVM-compatible wallet works. Use a wallet you control with strong seed phrase storage (hardware wallet preferred for any meaningful balance). Do not reuse a wallet that holds long-term cold storage; create a dedicated trading wallet for Hyperliquid activity to limit blast radius if anything goes wrong.

-

Acquire USDC on Arbitrum. This is the canonical deposit asset. Routes include: bridge from Ethereum mainnet using the official Arbitrum bridge, swap an existing Arbitrum asset to USDC through a DEX (Uniswap, Camelot, others), or withdraw USDC directly from a CEX that supports Arbitrum withdrawals (most major CEXs do). Confirm the network is Arbitrum One on every step. Wrong-network USDC sends are recoverable on some networks but the recovery path is technical and not guaranteed.

-

Connect to Hyperliquid and deposit. Open app.hyperliquid.xyz (note the frontend geo-block in restricted regions). Connect your wallet. Use the deposit function to bridge USDC from Arbitrum to the Hyperliquid L1. The deposit is a single transaction on Arbitrum, after which the USDC appears as available balance on the Hyperliquid frontend within a few minutes. Start with a small deposit to verify the round-trip path before scaling.

-

Start trading. The trading interface is similar in look and feel to a CEX futures interface. Select a pair (start with BTC or ETH for the deepest liquidity). Place limit orders to be a maker and earn the rebate, or market orders to take liquidity at the current best bid or ask. Set position size and leverage carefully; the 50x leverage cap on majors means a 2 percent adverse move on max leverage liquidates the position. Test withdrawal early in the trading workflow, ideally with a small amount, before scaling balances.

A few practical notes from observed user behavior. First, the funding rate is paid or received continuously rather than at fixed 8-hour intervals; check the live funding rate on each pair before holding a position overnight, as sustained-bias funding can erode position economics significantly. Second, the HLP vault is accessible from the same interface; if interested, allocate a small share to HLP for a month to understand the return profile experientially before committing larger capital. Third, consider HYPE staking once you have a stable trading workflow; the fee discount stacks meaningfully with volume tier discounts for active traders. Fourth, set wallet-level approvals carefully and revoke unused approvals periodically; this is general DeFi hygiene that applies on Hyperliquid as much as anywhere.

Bottom line

In 2026, Hyperliquid is the leading non-custodial perpetual-futures venue by most volume and execution-quality metrics, and the strongest no-KYC alternative to the major CEXs for retail traders running futures-focused strategies. The November 2024 HYPE TGE and the platform’s subsequent volume growth pushed it into the top 10 perpetual-futures venues globally, including against the major CEXs, and the order book quality on top pairs is now genuinely competitive with Bybit and Binance for retail-size flow.

The 8.4 out of 10 score breaks down like this. The platform earns the score through clean execution on top pairs, real self-custody and no-KYC access, a more aligned token model than the typical CEX utility token, and a clean operational track record through 2024-2026. The score is held below 9 by the shorter operating history, the validator set centralization, the bridge dependency, the lack of fiat on-ramp, the smaller asset list, and the higher learning curve relative to a CEX. The trade-offs are real and they cut both ways depending on the trader profile.

For a retail derivatives trader running size on top-pair perpetuals who values self-custody and no-KYC access, Hyperliquid is a credible primary venue in 2026 and we use it ourselves. For traders dependent on fiat on-ramps, spot markets, options markets, or the broader CEX product surface, the major CEXs remain the better primary venue, with Hyperliquid as a secondary specialty venue. For beginners new to crypto trading, the wallet-native learning curve makes Hyperliquid the wrong starting point; start on a CEX and add Hyperliquid to the stack once core workflows are established.

The risk shape is different from a CEX, not strictly lower. Self-custody removes one set of risks (platform-side custody failure) and adds another set (user-side wallet responsibility, smart-contract bridge risk, validator set centralization). The net risk profile is comparable to a major CEX in our assessment, with a different failure-mode distribution. Treat it accordingly: cap exposure, withdraw promptly, maintain wallet hygiene, and read the risk disclaimer before scaling capital.

Open account: Open Hyperliquid. See the affiliate disclosure for full detail. See our methodology for how we score every platform on the same framework.

Read next

- Hyperliquid vs Bybit. Direct side-by-side on fees, depth, custody model, and execution.

- Bybit review. The leading derivatives-focused CEX counterpart and direct comparison venue.

- Best no-KYC crypto exchanges 2026. The broader no-KYC landscape and where Hyperliquid sits.

- Methodology. How we evaluate platforms on a consistent framework.

- Risk disclaimer. Read this before depositing meaningful capital on any venue.

Frequently asked questions

Is Hyperliquid safe to use in 2026?

Hyperliquid is non-custodial, meaning user funds sit in self-controlled wallets rather than on an exchange balance sheet. There is no centralized custody risk in the Bybit or Binance sense. The real risks shift to smart-contract risk on the Arbitrum bridge, validator-set concentration on the Hyperliquid L1, and total user responsibility for wallet hygiene. Hyperliquid has operated without a major exploit through the 2024 TGE and 2025 expansion, but the protocol is younger and less battle-tested than the top CEXs. Loss of seed phrase means total loss with no recovery path.

What are Hyperliquid's fees?

Perpetual futures on top pairs charge approximately 0.025 percent taker and a 0.005 percent maker rebate at default tier. Volume-based discounts scale the taker fee down to roughly 0.013 percent at the highest tier. Staking HYPE further reduces taker fees through a separate discount layer. There are no gas fees for placing orders on the Hyperliquid L1 (the chain is purpose-built for the order book). Bridge deposits and withdrawals from Arbitrum incur standard L2 gas, plus a small protocol fee on the withdrawal side.

Do I need KYC for Hyperliquid?

No. Hyperliquid is fully non-custodial and does not request KYC at the protocol level. Account creation is a wallet connection, not an identity verification flow. The frontend at app.hyperliquid.xyz geo-blocks certain jurisdictions (notably US IPs) but this is a frontend restriction, not a protocol restriction. There is no email, no government ID, no liveness check, no source-of-funds questionnaire. For privacy-focused traders this is the cleanest no-KYC perp venue currently operating at meaningful liquidity depth.

Can US users use Hyperliquid?

The frontend at app.hyperliquid.xyz geo-blocks US IP addresses. The protocol itself is permissionless and there is no on-chain enforcement of geographic restrictions. Many US users access the platform through VPNs or alternative frontends; this is a personal compliance decision and carries the same regulatory consideration as any other US user accessing an offshore non-licensed venue. We do not advise it. US users seeking a regulated path should look at CME futures, Coinbase, or Kraken.

What is the HYPE token?

HYPE is Hyperliquid's native token, launched on November 29, 2024 in one of the largest community airdrops in crypto history. Roughly 28 percent of the genesis supply went directly to early users and traders, with the team and ecosystem receiving smaller allocations than typical VC-backed launches. HYPE powers fee discounts when staked, secures the Hyperliquid L1 through validator staking, and accrues value through a protocol-level buyback mechanism funded by trading fee revenue. The TGE distribution model became a reference point for community-first token launches in 2025.

How does Hyperliquid compare to Bybit and Binance perps?

On top pairs (BTC, ETH, SOL), Hyperliquid's order book quality is now competitive with Bybit and Binance in spread tightness and depth at the top of book. Where Hyperliquid wins: no KYC, self-custody, lower fees at retail volume, and meaningful HYPE token alignment. Where it loses: thinner liquidity on long-tail altcoins, no spot market for most assets, no fiat on-ramp, steeper learning curve for wallet-native users. For sophisticated derivatives traders running size on top pairs, Hyperliquid is a credible primary venue in 2026. See our [Bybit review](/blog/bybit-review/) for the CEX counterpart comparison.

What is the HyperBFT consensus?

HyperBFT is the consensus algorithm powering the Hyperliquid L1, the purpose-built blockchain that hosts the order book. It is a Byzantine Fault Tolerant variant optimized for low-latency order-matching workloads, with sub-second block times and an architecture that batches order book operations directly into consensus rather than treating trades as generic smart-contract calls. The result is that placing, canceling, and matching orders on Hyperliquid feels closer to a centralized matching engine than a typical DEX. This is the technical foundation that makes the CLOB design viable.

How do withdrawals work on Hyperliquid?

Deposits arrive on the Hyperliquid L1 by bridging USDC from Arbitrum. Withdrawals reverse the path: assets exit the L1 back to Arbitrum, then can be moved to Ethereum mainnet or other networks via standard L2 bridges. The bridge contract on Arbitrum is the primary smart-contract risk surface; it has been audited but remains the single largest dependency in the security model. Withdrawal processing on the L1 side is near-instant; finality on the Arbitrum bridge side typically takes a few minutes depending on network conditions.

#Hyperliquid#DEX#perpetuals#HYPE#no-KYC#self-custody#L1

Discussion

Loading comments…